AI Stock Sell-Off: What Triggered the Panic?

The Big Short 2.0? More Like a Calculated Wager

Michael Burry, the man who made a fortune betting against the housing market in 2008 (a move immortalized in "The Big Short"), is now shorting AI stocks. Specifically, Nvidia and Palantir. The news triggered a tech sell-off, with major indices in Asia taking the biggest hit. Japan's Nikkei 225 closed down 2.5%, led by a SoftBank plunge of over 10%. Is this a repeat of the housing bubble, or is Burry playing a different game this time around? Trader who inspired The Big Short sets off AI tech share sell-off

AI Hype vs. Financial Reality

The market's been riding the AI wave hard. Many jumps in tech shares have been linked to major investments in firms. Amazon shares hit an all-time high after announcing a $38 billion deal with OpenAI. But the question isn't whether AI is revolutionary, but whether these valuations are sustainable. And that's where Burry's bet comes into play.

Burry's firm, Scion Asset Management, disclosed a $1.1 billion short position against Nvidia and Palantir. Palantir, in particular, is a lightning rod. Its CEO, Alex Karp, called Burry's move "batshit crazy," pointing to Palantir's recent Q3 revenue gain of $1.2 billion, up 63%. But let's look closer. A 63% increase is impressive, but that's against a base. Palantir's projected annual revenue is $4.4 billion. Its market cap? $450 billion. That's a price-to-sales ratio of over 100. Is that justified, even for a company growing as fast as Palantir?

The market is highly vulnerable to a selloff in tech stocks. In October, tech stocks tracked by Bank of America contributed more than 90% of the S&P 500’s total return for the month. The Magnificent Seven stocks alone contributed 80%. The question is whether this concentration of value is sustainable.

A Broader Market Correction?

It's not just Palantir. Nvidia, despite being the first company to hit a $5 trillion valuation, dropped nearly 4% after Burry's bet was revealed. SoftBank, a major investor in AI development, suffered one of its steepest drops. The market is starting to question whether these companies are overspending on AI without sufficient returns. As Farhan Badami from eToro notes, "Spending within AI-focused tech firms has been really high, and for some companies, they are not making enough money to justify the spending."

But here's where I think the comparison to 2008 breaks down. The housing bubble was fueled by systemic risk – bad loans bundled and resold, creating a house of cards. This feels different. It's more like a correction of exuberance. Are valuations stretched? Almost certainly. Is there systemic risk baked into the AI market? Details on that remain scarce, but it appears not nearly to the same extent. I've looked at hundreds of these filings, and the level of interconnectivity that caused the 2008 collapse simply isn't there.

It's also worth considering the psychology at play. Burry's tweet – "Sometimes, we see bubbles. Sometimes, there is something to do about it. Sometimes, the only winning move is not to play" – is a clear attempt to influence market sentiment. Is he right? Time will tell. But the fact that a single tweet from a well-known investor can trigger a global sell-off suggests that the market's confidence in AI valuations is fragile.

This Isn't 2008, It's Just Math

Burry's bet isn't about predicting a complete collapse of the AI industry. It's about recognizing that valuations have outpaced reality. It's a calculated wager that the market will eventually correct itself, and that those who are currently overpaying for AI stocks will be left holding the bag.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

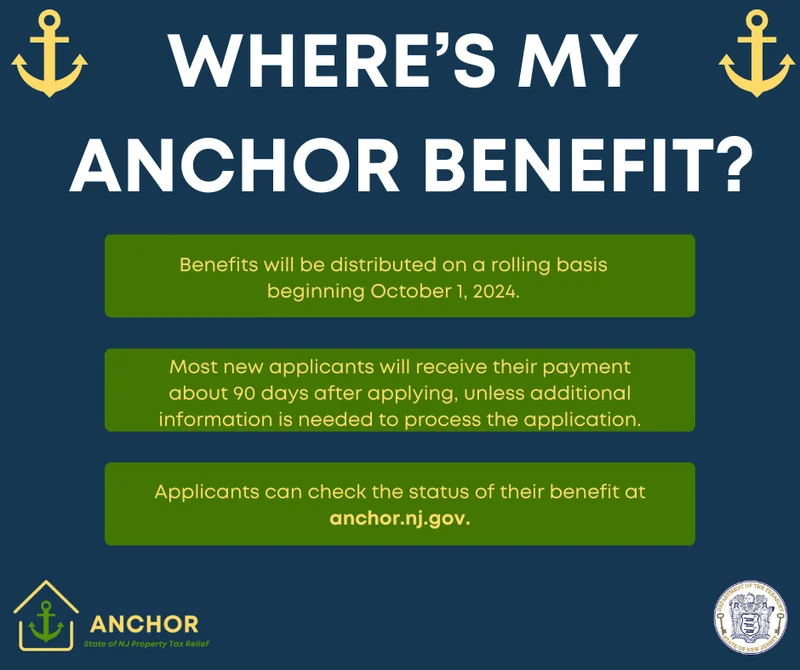

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

Zcash's Zombie Rally: The Price Prediction vs. What Reddit Is Saying

So,Zcashismovingagain.Mytime...

- Search

- Recently Published

-

- Google Stock: Unlocking Its Next Frontier Alongside Nvidia, Meta, and Amazon

- 5G: What's the deal with Verizon, T-Mobile, and those '5G' phones?

- Monero: Price, Privacy, and The Data Reddit Isn't Discussing

- Bitcoin: Its Explosive Surge and the Future It's Building

- Meteora: The $1 Billion Valuation and What You're *Not* Being Told

- BMO: The Data on Its Banking Services & Access Points

- CNN's "Flying Car" Story: The Hype vs. The Absurd Reality

- Newcastle Beats Athletic Bilbao: The Match Results and All The Sudden Hype

- The Sonder-Marriott Identity Crisis: Why This 'Partnership' Is a Complete Mess

- Stimulus Check 2025: What's the Buzz and Could Trump Be Involved?

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- Plasma (5)

- Zcash (5)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- bitcoin price (3)

- SX Network (3)

- Monero (3)