Vertex's Journavx Launch: Hype vs. Reality

Vertex Pharmaceuticals is making noise about its non-opioid pain reliever, Journavx. During their recent Q3 presentation, they touted prescription numbers and hospital formulary additions, painting a picture of successful adoption. But as always, the devil's in the details. Let's dissect the numbers and see if this launch is truly a game-changer or just a well-spun narrative.

Journavx: The $20 Million Question

The headline figure is Journavx's $20 million in sales for the quarter. That's $3 million short of analyst consensus. Not a catastrophic miss, but a miss nonetheless. And it wasn’t just Journavx. Alyftrek, their cystic fibrosis treatment, and Casgevy, the sickle cell gene therapy, also underperformed, falling short of expectations by $10 million and a more concerning $25 million, respectively (that’s a hefty difference of -59.52% from projections). The market reacted predictably; Vertex's share price dipped 5% in premarket trading.

Vertex is trying to counter this with positive metrics: over 300,000 prescriptions filled this year, 750 hospitals adding Journavx to their formularies, and reimbursement policies covering 170 million people. They’re highlighting the broad range of doctors prescribing it – orthopedic surgeons, plastic surgeons, dentists, the whole nine yards.

But here's where the "so what?" factor kicks in. Filling prescriptions is one thing; sustained usage and repeat prescriptions are another. Adding a drug to a formulary is a victory, but it doesn't guarantee it will be the preferred option. And 170 million covered lives sounds impressive, but how many of those people will actually use Journavx, especially given its price point?

The company claims Journavx is being used in a wide range of pain settings, from joint replacements to dental procedures. But without knowing the volume of prescriptions for each setting, it's impossible to gauge where the real demand lies. Are dentists driving the bulk of prescriptions, or are orthopedic surgeons? This granularity is crucial for understanding the drug's true potential.

The Opioid Alternative: A Pricey Proposition

The elephant in the room is cost. At $15.50 per 50-mg dose, Journavx is significantly more expensive than generic opioids, which cost around $0.50. This price discrepancy is a major hurdle, especially in a healthcare system where cost is a primary consideration.

Vertex is betting on the NOPAIN Act to improve Medicare coverage and increase access to non-opioid pain management. But government shutdowns and bureaucratic delays are notorious for derailing even the best-laid plans. And even with improved coverage, will doctors and patients be willing to pay a premium for Journavx, especially when cheaper alternatives exist?

I've looked at hundreds of these quarterly reports, and the emphasis on prescription numbers without corresponding revenue growth always raises a red flag. It suggests either a high rate of initial prescriptions that aren't being refilled, or that the dosage per script is lower than anticipated. Either way, it's a potential warning sign.

Vertex needs a strong Q4 to hit Citi's $110 million sales projection for 2025. Given the current trajectory, that seems like a tall order. While the company expresses "high confidence" in the unmet need for non-opioid pain relief, confidence doesn't pay the bills. Results do.

Early Hype, or Real Momentum?

Vertex is trying to sell a narrative of strong adoption and future growth for Journavx. The prescription numbers are certainly eye-catching. But beneath the surface, the sales figures tell a different story. The key question now is whether Vertex can translate those initial prescriptions into sustained revenue growth and prove that Journavx is more than just a flash in the pan.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

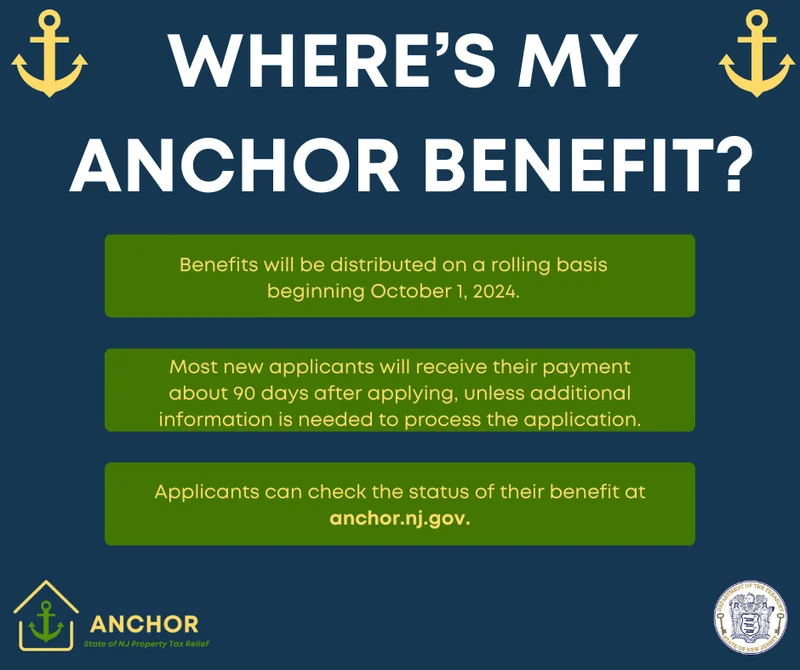

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

Zcash's Zombie Rally: The Price Prediction vs. What Reddit Is Saying

So,Zcashismovingagain.Mytime...

- Search

- Recently Published

-

- Google Stock: Unlocking Its Next Frontier Alongside Nvidia, Meta, and Amazon

- 5G: What's the deal with Verizon, T-Mobile, and those '5G' phones?

- Monero: Price, Privacy, and The Data Reddit Isn't Discussing

- Bitcoin: Its Explosive Surge and the Future It's Building

- Meteora: The $1 Billion Valuation and What You're *Not* Being Told

- BMO: The Data on Its Banking Services & Access Points

- CNN's "Flying Car" Story: The Hype vs. The Absurd Reality

- Newcastle Beats Athletic Bilbao: The Match Results and All The Sudden Hype

- The Sonder-Marriott Identity Crisis: Why This 'Partnership' Is a Complete Mess

- Stimulus Check 2025: What's the Buzz and Could Trump Be Involved?

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- Plasma (5)

- Zcash (5)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- bitcoin price (3)

- SX Network (3)

- Monero (3)